Tired of Financial Stress keeping you awake? Discover our powerful 5-step plan to break the anxiety cycle, regain control of your money, and unlock deeper sleep and better health for good.

There’s a particular kind of 3 a.m. that only people with money problems know. You’re staring at the ceiling, running numbers in your head that don’t add up, replaying a purchase you regret, or dreading a bill you’re not sure you can pay.

The house is quiet, but your mind is not. And the worst part? You’re exhausted, but you can’t sleep.

If that sounds familiar, you’re not alone. Financial stress is one of the most common, most underestimated sources of anxiety in modern life.

It doesn’t announce itself dramatically. It hides in avoided bank statements, in the tight feeling in your chest when your phone rings from an unknown number, in the way you brace yourself every time you check out at the grocery store.

And over time, that constant background hum of money worry does something most people don’t realize: it quietly dismantles your health.

This article is written for anyone who’s living somewhere between “I’m managing” and “I’m barely holding on.” You don’t need to be in financial ruin to feel financial stress.

Most people who struggle with it are trying their best; they’re just overwhelmed, unsure where to start, and tired of advice that feels out of reach.

What follows is a practical, honest, human guide to reducing financial stress, not by becoming wealthy overnight, but by reclaiming a sense of control that lets you breathe again.

Quick Summary

What this article covers:

- Why financial stress affects your physical and mental health more than you may realize

- The five hidden ways money worries are disrupting your sleep

- Seven evidence-backed strategies to reduce financial stress starting today

- How to build lasting habits around financial calm, not just financial improvement

- Simple mindset shifts that make a real difference even before your finances change.

Who this is for: Anyone feeling overwhelmed by debt, income insecurity, unclear financial goals, or the daily weight of money anxiety.

Bottom line: You don’t need to fix your finances completely to reduce financial stress. You need a plan, a few small wins, and a shift in how you relate to money.

The Link Between Financial Stress and Health: What You Need to Know

Most people treat financial stress as a money problem. But your body treats it as a threat.

When you’re worried about money, whether it’s a missed payment, a shrinking savings account, or an uncertain income, your nervous system responds the same way it would to a physical danger.

Cortisol and adrenaline rise. Your heart rate increases. Your muscles tighten. This stress response evolved to help us escape predators, not to survive monthly budgets, but the body doesn’t know the difference.

The problem is that financial stress isn’t a one-time event. It’s chronic. And chronic stress is where the real health damage occurs.

Research consistently links financial stress to a wide range of physical and mental health conditions: disrupted sleep, elevated blood pressure, weakened immune function, digestive problems, headaches, and a significantly higher risk of anxiety and depression.

When you’re financially stressed for months or years, your body rarely gets the chance to fully recover. The stress response stays partially activated, and the wear and tear builds.

The Powerful Link Between Money Habits and Mental Health

There’s a reason financial advisors and therapists increasingly work together. The relationship between financial behavior and mental health is deeply bidirectional.

Financial stress causes anxiety and depression, but anxiety and depression also make financial decision-making harder. They push us toward avoidance, impulse spending, or paralysis. It becomes a loop.

What’s particularly striking is that it’s not just people with serious debt who suffer. Studies show something surprising. You don’t need to be in real financial trouble to feel its effects. Simply feeling financially insecure can be just as damaging.

Even if you’re technically stable, the worry alone is enough. Your mind and body respond as if the hardship is real.

The stress comes from uncertainty and lack of control, not necessarily from a specific dollar amount.

This matters because it means that improving how you relate to your finances, building a clearer picture, setting small goals, and reducing uncertainty can meaningfully reduce stress even before your bank balance changes significantly.

The Broader Impacts: Productivity, Employment, and Well-being

Financial stress doesn’t stay at home when you go to work. It follows you. Money stress doesn’t stay at home. It follows you straight to work. Research on financial well-being in the workplace makes this clear.

Employees dealing with significant financial stress become less productive. They find it harder to focus. They take more sick days. And when pressure builds, they’re more likely to make poor decisions.

It also affects relationships. Money is consistently cited as one of the top causes of relationship conflict.

The tension it creates between partners, the shame it breeds in silence, and the social withdrawal it encourages all compound the psychological burden well beyond the financial facts themselves.

Understanding this helps explain why reducing financial stress isn’t just about having more money.

It’s about restoring something essential: your capacity to think clearly, connect with others, rest properly, and function as a full person rather than just a person managing a crisis.

The Vicious Cycle: How Financial Stress Damages Your Sleep and Health

Sleep and financial stress are locked in a feedback loop that can feel nearly impossible to break, once you’re in it.

When you’re stressed about money, sleep is one of the first casualties. Racing thoughts, anxiety, and elevated cortisol all interfere with the ability to fall asleep and stay asleep.

You may find yourself waking at 2 or 3 a.m., your mind immediately jumping to unpaid bills or financial decisions you’re dreading. This is not a character flaw. It’s biology.

But here’s where the cycle turns vicious: poor sleep dramatically worsens your ability to manage stress.

It impairs the prefrontal cortex, the part of your brain responsible for rational decision-making, impulse control, and emotional regulation.

When you’re sleep-deprived and financially stressed, you are literally less capable of making good financial decisions. You’re more reactive, more prone to avoidance, and less able to think long-term.

Sleep deprivation also raises cortisol further, increasing anxiety and making it harder to tolerate uncertainty. And financial situations are inherently uncertain.

The physical consequences compound this. Chronic poor sleep has been linked to weight gain, weakened immunity, increased risk of type 2 diabetes and cardiovascular disease, hormonal disruption, and accelerated cognitive decline.

These aren’t distant risks; they are measurable effects of sustained sleep disruption.

Understanding the cycle is step one. Breaking it requires addressing both sides: improving your relationship with money and actively protecting your sleep, even while the financial situation is still being worked on. These two things are not separate.

5 Ways Financial Stress Is Keeping You Up at Night

Debt and Financial Obligations

Debt has a particular psychological weight that goes beyond the numbers. It doesn’t just sit in your bank account; it sits in your head.

The awareness that you owe money, that interest is accumulating while you sleep, that missing a payment has consequences, all of this creates a baseline level of anxiety that rarely fully quiets.

For many people, debt avoidance becomes a coping mechanism. They stop checking their balances, stop opening statements, and stop doing the math. This avoidance feels like relief in the short term, but creates a worse problem.

The debt continues to grow in the background, while the anxiety of not knowing exactly how bad it is adds its own layer of stress.

The antidote to this particular form of stress is not to eliminate debt overnight, but to face it clearly. When you know the exact numbers, you have something to work with. Uncertainty is almost always more stressful than difficult facts.

Lacking Financial Security

Financial insecurity doesn’t require debt. Millions of people who are technically “in the black” feel a constant low-grade anxiety because they have no buffer. No emergency fund. No savings cushion.

One unexpected expense, a car repair, a medical bill, a broken appliance, and the whole financial situation becomes a crisis.

Living without a financial cushion means living in a permanent state of vulnerability. Every unexpected event is a threat. And the nervous system, wired to protect you, responds accordingly: with hypervigilance, low-grade anxiety, and difficulty relaxing.

Building financial security starts small. Even a few hundred dollars in a dedicated emergency account creates a psychological buffer before it creates a financial one. The relief is real and measurable.

Money Worries and Anxiety

Generalized financial anxiety is different from having specific money problems. It’s the habit of worry, the mind that defaults to money concerns, that anticipates financial problems before they exist, that interprets neutral events through the lens of financial threat.

This type of anxiety often has roots that go beyond present circumstances. It can develop from growing up in financial instability, from a past financial crisis, or from watching parents struggle. It becomes a lens rather than a response. And that lens is always on.

Managing financial anxiety is partly a financial task and partly a mental health task. Both deserve attention.

Unclear Financial Goals

When you don’t know what you’re working toward financially, progress feels impossible because you can’t measure it. The absence of clear goals creates a formless anxiety where everything feels equally urgent and equally overwhelming.

Unclear financial goals also make spending harder to regulate. Without a clear picture of your priorities, it’s difficult to make confident choices about what to spend and what to save. And that difficulty breeds guilt, second-guessing, and more stress.

Setting even one clear financial goal, however modest, gives you direction. It turns an overwhelming situation into a path.

Overspending and Financial Regrets

Overspending and the regret that follows it create a particularly corrosive cycle. Emotional spending often occurs in response to stress; it’s soothing in the moment. But the financial consequences create additional stress, which can lead to increased emotional spending.

The guilt and shame attached to financial regrets are worth acknowledging directly. They are among the most common hidden contributors to financial stress, and they are rarely helped by self-criticism.

What helps is understanding the trigger, developing alternative responses, and learning to distinguish between spending that serves you and spending that costs you more than money.

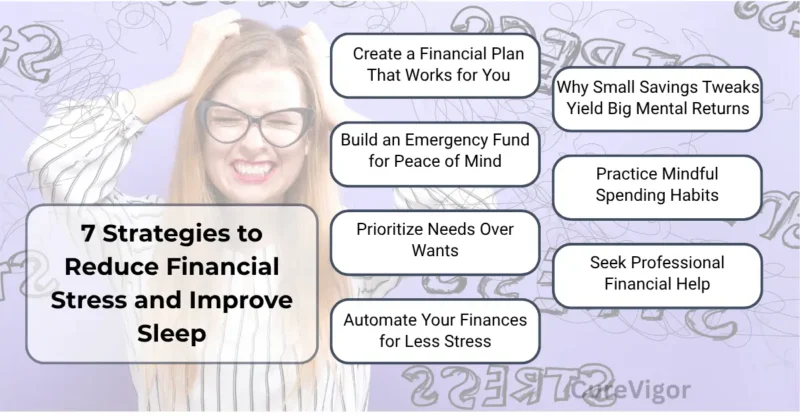

7 Strategies to Reduce Financial Stress and Improve Sleep

Create a Financial Plan That Works for You

The single most effective thing most people can do to reduce financial stress is to create a clear, honest picture of their financial situation, income, expenses, debt, and savings- and build a simple plan around it.

A financial plan doesn’t need to be complex. It needs to be honest and realistic. It should reflect your actual life, not an idealized version.

That means accounting for irregular expenses, for subscriptions you actually use, for the coffee you genuinely enjoy. Budgets that feel like punishment are budgets that get abandoned.

Start with clarity: write down what comes in and what goes out each month. Then identify the two or three areas with the most room to adjust.

Small, realistic changes, made consistently, reduce financial stress more reliably than dramatic overhauls that collapse after two weeks.

The planning process itself reduces anxiety. Uncertainty is one of the biggest drivers of financial stress, and a plan, even an imperfect one, reduces uncertainty.

Build an Emergency Fund for Peace of Mind

If there’s one financial habit that has the most direct effect on psychological well-being, it’s having an emergency fund. Even a small one.

The function of an emergency fund is not primarily mathematical; it’s emotional. It means that when something goes wrong, it’s a problem, not a crisis.

That distinction, between a problem you can handle and a crisis that upends everything, is the difference between manageable stress and overwhelming panic.

Start wherever you are. If you can set aside $25 a month, start there. Automate it so it happens without requiring a decision each month.

Watch the number grow. This is one of the clearest, most tangible ways to feel more in control of your financial life.

Prioritize Needs Over Wants

This piece of advice is often given in a way that feels harsh or moralistic, but it doesn’t have to be.

Understanding the difference between needs and wants and making deliberate choices about both is fundamentally about aligning your spending with your actual priorities, not about depriving yourself.

The question isn’t “Is this a luxury?” The question is “Does this spending reflect what I actually value, or is it happening on autopilot?”

Many people find that when they examine their spending with real curiosity rather than judgment, they discover purchases that don’t actually make them happy, and letting those go doesn’t feel like a sacrifice. It feels like clarity.

This clarity is a stress reducer. Intentional spending, even when money is tight, creates a sense of agency. Unconscious spending, by contrast, creates regret and a sense of powerlessness.

Automate Your Finances for Less Stress

Every financial decision you have to make manually is a potential moment of procrastination, avoidance, or error. Automation reduces the cognitive load of managing money, and lower cognitive load means lower stress.

Automating your savings means money moves before you have a chance to spend it.

Automating bill payments means you don’t carry the mental weight of remembering due dates.

Setting up automatic debt payments, even at the minimum while you build toward more, means one less thing living in the back of your mind.

The psychological relief of knowing your financial basics are handled, that you’re not going to accidentally miss a payment, that your savings are growing without effort, is genuinely significant.

Automation is one of the most underused tools for reducing stress in personal finance.

Why Small Savings Tweaks Yield Big Mental Returns

There’s a disproportionate psychological return on small financial improvements. Moving from saving nothing to saving $50 a month produces more measurable relief than moving from saving $1,000 a month to saving $1,100.

The early gains in financial security are where the biggest psychological shifts happen.

This is important to understand because it means you don’t have to wait until you’re financially comfortable to feel less financially stressed.

The act of moving in the right direction, even slowly, even by small amounts, signals to your nervous system that things are improving. That signal matters.

Celebrate small wins without dismissing them. They are not just stepping stones. They are, in themselves, meaningful.

Practice Mindful Spending Habits

Mindful spending is not about spending less, though it often leads to that. It’s about spending more consciously, pausing before purchases, checking in with yourself about what you’re actually seeking, and making choices that reflect your real priorities.

One simple practice: for any non-essential purchase over a certain amount, give it 24 to 48 hours before making the purchase. Not to torture yourself with indecision, but to give the initial impulse time to settle so you can make a clearer choice.

Many purchases that feel urgent in the moment feel unnecessary a day later.

Another practice: periodically review your spending with curiosity rather than judgment

Look at where your money actually went last month and notice whether it matches your stated priorities. This awareness, honest and non-punishing, is the foundation of financial behavior change.

Seek Professional Financial Help When Needed

There’s a particular kind of shame that surrounds seeking financial help. The cultural message is that capable adults should be able to manage their own money without assistance. That message is not only wrong — it’s actively harmful.

Financial advisors, credit counsellors, and financial therapists exist because money is genuinely complicated, and because our relationship with it is shaped by psychology, history, and habits that go well beyond spreadsheet skills.

Seeking professional guidance is not an admission of failure. It’s one of the most effective things you can do.

If cost is a barrier, there are free and low-cost resources available: nonprofit credit counselling agencies, financial literacy programs, and online tools designed to help people at every income level. The first step is often just acknowledging that you don’t have to figure this out alone.

Accessible Habits, No Matter Your Financial Situation

One of the most frustrating things about standard financial advice is how inaccessible it can feel. “Build a six-month emergency fund.”

“Max out your retirement contributions.” “Invest the difference.” These are fine goals, but they’re useless as starting points for someone who is genuinely struggling.

Reducing financial stress doesn’t require a high income. It requires any of the following: a little more clarity, a little more intention, one less source of uncertainty, or one small decision made with your actual values in mind.

If you’re living paycheck to paycheck, the goal isn’t to follow a conventional financial plan. The goal is to find one thing, just one, that gives you a slightly better sense of control.

That might be knowing your exact account balance instead of guessing. It might be a call to ask about a payment plan on a medical bill. It might be setting a $10 automatic savings transfer.

Whatever is accessible to you right now is enough to start with. Progress is progress at any scale.

How to Start Saving and Paying Off Debt Consistently

Consistency matters more than intensity. A $50 monthly savings habit maintained for three years will do more for your financial and psychological well-being than a $500 burst that collapses after two months.

The practical key to consistency is reducing friction. That means automating what you can, keeping your financial systems simple, and building habits that don’t require willpower to maintain. Willpower is finite. Systems are more reliable.

When it comes to paying off debt, two approaches dominate personal finance advice. The first is the avalanche method. This means paying off your highest-interest debt first.

It’s the mathematically optimal choice and saves you the most money over time. The second is the snowball method.

This means tackling your smallest balance first. It may cost a little more in interest, but it delivers early wins. And those early wins build momentum.

Neither is universally superior. The right one is the one you’ll actually stick to, which often means the snowball, because the early wins build momentum.

Focus on Financial Progress, Not Perfection

Perfectionism is one of the quieter drivers of financial avoidance.

When people feel they’ve made a mistake, overspent, missed a payment, or deviated from the budget, they often respond not by correcting course but by giving up entirely.

The logic, unconsciously, is “I’ve already failed, so why bother?”

This is worth naming and resisting directly. Financial progress is not linear. There will be months where you spend more than planned, unexpected expenses that derail your budget, and decisions you wish you’d made differently. None of this erases progress.

What matters is the trend over time, not the performance in any given week. Tracking your financial progress, even loosely, helps you see that trend.

A simple spreadsheet showing your savings balance or total debt over time makes the trajectory visible. Visible progress sustains motivation in ways that willpower alone cannot.

Cultivating Calm: Improving Sleep and Health Amidst Financial Realities

Reducing financial stress and improving sleep are mutually reinforcing, but they don’t have to wait on each other. You can take steps to protect your sleep even while you’re still working through financial challenges.

A few practices that genuinely help:

Create a financial boundary around bedtime. Avoid reviewing your finances, paying bills, or engaging in financial planning in the hour before you sleep.

Your brain needs time to shift out of problem-solving mode before it can rest. Schedule your financial review for a specific, bounded time earlier in the day instead.

Write it down before bed. If financial worries surface at night, as they reliably do, try keeping a notepad by your bed.

Write down what’s worrying you and, if possible, one small action you can take tomorrow. This creates a sense of closure, allowing the brain to set the thought down rather than cycling through it.

Address the physical side of stress. Regular physical activity, even a 20-minute walk, meaningfully reduces cortisol levels and improves sleep quality.

Deep breathing, progressive muscle relaxation, and mindfulness practices have solid research support for reducing both anxiety and sleep disruption.

These are not luxuries; they are stress-management tools that cost nothing.

Limit alcohol. Many people use alcohol to manage financial anxiety. While it may initially aid sleep onset, alcohol disrupts sleep architecture, particularly the deep, restorative stages, and typically worsens sleep quality in the second half of the night.

It also tends to increase anxiety the following day, creating a cycle.

Sustaining Your Journey: Long-Term Financial Wellness for Enduring Health

The goal of reducing financial stress isn’t a destination you arrive at once your finances are perfect.

It’s a relationship you develop with money over time, one characterized by increasing clarity, intentionality, and self-compassion.

Long-term financial wellness looks like this: You know roughly where you stand at any given time. You have a sense of your priorities.

You have some buffer, however modest, against unexpected events. You make decisions about money that generally reflect your values, even when those decisions aren’t perfect.

And when things go sideways, as they will, you have enough trust in your own ability to course-correct that it doesn’t spiral into catastrophe.

This is within reach for most people, not immediately, not without effort, but genuinely within reach. The path is not smooth. But it is navigable.

A few things worth sustaining over the long term:

Regular financial check-ins, monthly is ideal, quarterly at minimum, keep you connected to your financial reality without being consumed by it. Think of these as maintenance, not crisis management.

A consistent savings habit, however small, maintained through good times and difficult ones, builds both a financial cushion and psychological resilience. The habit itself becomes a form of self-trust.

A willingness to adjust your budget, your goals, and your approach when circumstances change. Flexibility is not the same as giving up. It’s what makes long-term commitment possible.

And finally: community. Financial stress is worsened by shame and isolation. Finding others who are working on similar challenges, whether through a financial counsellor, a trusted friend, an online community, or a book, reduces the sense that you’re carrying this alone. You’re not.

The Bottom Line: Embrace Your Confident, Stress-Reduced Future

Financial stress is real, common, and serious. But it is not permanent, and it is not something you have to simply endure.

The strategies in this article are not about achieving financial perfection. They are about reducing the uncertainty, avoidance, and helplessness that make financial stress so damaging to your sleep, your health, your relationships, and your quality of life.

You don’t need to fix everything at once. You need to start somewhere, with a clearer picture, one small step, one habit that moves you slightly in the right direction. That is enough to begin feeling better. And feeling better is enough to make the next step easier.

The 3 a.m. ceiling-staring doesn’t have to be permanent. With the right approach, honest, practical, and compassionate toward yourself, a calmer relationship with money is genuinely possible. Not someday. Starting now.

If you’re experiencing significant financial hardship, consider reaching out to a nonprofit credit counselling agency or a financial therapist. Help is available, and asking for it is one of the most effective things you can do.

Read more articles about Health & Wellness Tips.

You might like to read: