Learn how to assess company financial health, analyze key metrics, improve cash flow, and strengthen long-term stability with practical steps.

A business can look busy and still be in trouble.

How to Assess The Financial Health of Your Company

Orders are coming in, and clients are replying. Revenue looks decent on paper. The team is working hard. From the outside, everything seems fine. But inside the numbers, a different story may be developing.

Cash may be too tight. Margins may be shrinking. Debt may be growing quietly in the background.

And that uneasy feeling in your chest every time payroll, rent, or supplier payments come due is often the first real sign that something is off.

That is why checking your business’s financial health matters so much.

Business owners often wait too long to look deeply at the numbers because they are busy running the business itself.

That is understandable, but dangerous. A company rarely collapses because of a single dramatic event overnight.

More often, it weakens gradually through ignored trends, poor cash flow control, delayed reporting, and decisions made without a clear financial picture. The business may still be operating, but not from a position of strength.

A proper company financial health check helps you see whether your company is stable, efficient, resilient, and able to grow without constant strain.

It gives you a clearer answer to one of the most important questions any owner can ask: Is this business truly healthy, or just active?

Quick Summary Box

- Company financial health means: how well your company generates cash, manages obligations, protects margins, and stays stable over time.

- The best way to check it is to review your financial statements, analyze cash flow, study revenue and profitability trends, and assess financial risk exposure.

- Key warning signs: rising revenue but poor cash flow, shrinking margins, late payments, growing debt, and overdependence on a few clients.

- Key metrics to review: current ratio, gross profit margin, net profit margin, operating cash flow, debt-to-equity, and receivables turnover.

- How often to review: monthly for a quick check, quarterly for deeper analysis, and annually for strategic planning.

This guide will help you understand company financial health, evaluate it step by step, spot red flags early, and strengthen your financial decision-making.

What This Guide Covers

This article explains what company financial health really means, why it matters, and how to evaluate it in a practical way.

You will walk through four core steps: conducting a full financial analysis, evaluating cash flow management, analyzing revenue and profitability trends, and assessing financial risk exposure.

You will also learn which financial statements matter most, what key metrics to watch, how to do a regular business check-up, what red flags to take seriously, and what common mistakes small business owners make when judging performance.

If you want a broader understanding of the concept itself, you can also connect this article to your pillar guide, Financial Health Defined: How to Measure and 7 Tips to Improve Your Own, which covers the wider meaning of financial health beyond business numbers.

What Is Company Financial Health?

A company’s financial health is the overall strength and stability of a company’s finances. It reflects whether the business can cover its obligations, generate enough cash, stay profitable, manage risk, and continue operating without constant financial stress.

A financially healthy business does not need to be huge. It does not need explosive growth. It does not need perfect margins every month.

What it needs is balance. It needs enough cash to operate, enough profit to justify the effort, enough structure to survive setbacks, and enough clarity to make smart decisions.

This is important because growth alone does not prove financial health. A business can grow revenue while becoming weaker underneath. Sales can rise while cash flow falls. Expenses can expand faster than margins.

A company can look successful from the outside while becoming more fragile every quarter. Humans do adore confusing “more” with “better.” It keeps consultants employed, at least.

Company Financial Health vs Business Growth

Growth and financial health often support each other, but they are not the same thing. Growth is about expansion. Financial health is about stability and sustainability.

A business can grow too fast, hire too quickly, overstock inventory, offer loose payment terms, or take on debt before the foundation is ready. In that case, growth creates pressure instead of strength.

A smaller business with steady cash flow, disciplined expenses, and healthy margins may actually be in a much stronger position than a larger one that is constantly stretched.

Why Checking Financial Health Matters

Checking financial health helps you make better decisions before problems become urgent.

It gives you a clearer understanding of what the business can safely afford, where the pressure points are, and what changes need attention now rather than later.

It also matters for credibility. If you ever want financing, investors, strategic partners, or even just calmer internal planning, you need more than vague optimism.

You need numbers that make sense. A lender, investor, or serious advisor is not impressed by “we’re doing well, mostly.” They want evidence.

Most importantly, regular financial review helps you catch patterns early. A business usually sends warning signs before a real cash crisis arrives.

If you pay attention to those signals, you have choices. If you ignore them, decisions become reactive, expensive, and rushed.

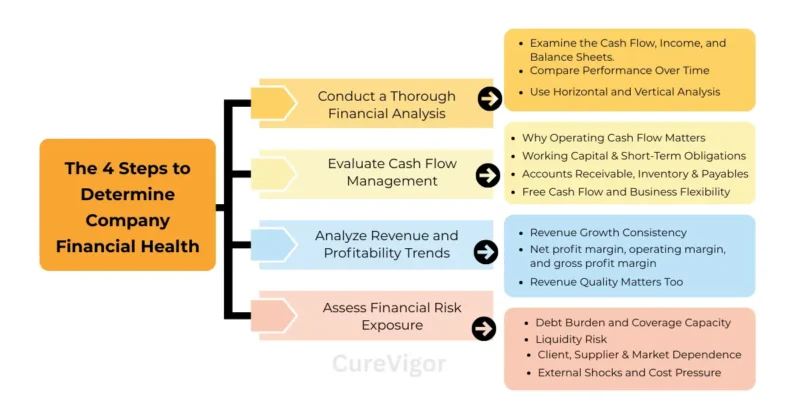

The 4 Steps to Determine Company Financial Health

The most useful way to evaluate a business’s financial health is through four interconnected steps. Each one tells part of the story. Together, they give you a more complete picture.

1. Conduct a Thorough Financial Analysis

The first step is to carefully review the main financial statements. Too many owners look only at sales totals or bank balance snapshots. That is not enough. You need to understand the business’s full financial structure.

Examine the Cash Flow, Income, and Balance Sheets.

Start with the income statement. This shows revenue, expenses, and profit over a period of time. It helps you answer whether the business is actually earning money after costs are accounted for.

Then review the balance sheet. This shows what the business owns, what it owes, and what is left over as equity. It gives you a snapshot of financial position rather than performance over time.

Finally, review the cash flow statement. This shows how cash is actually moving through the business.

It separates operating, investing, and financing activities. This is where many businesses discover the uncomfortable truth that profit and cash are not the same thing.

Together, these three statements tell you whether the business is profitable, liquid, leveraged, and financially stable.

Compare Performance Over Time

A single month or quarter rarely tells the whole truth. Financial health should be checked in trends, not isolated moments.

Compare current performance to previous months, previous quarters, and the same period last year.

Ask basic but important questions. Is revenue becoming more consistent? Are expenses rising faster than sales?

Are margins improving or tightening? Is debt increasing? Is cash becoming more strained even though revenue is up?

Trend analysis matters because slow deterioration often hides inside acceptable-looking numbers. A business can seem fine until you compare five quarters side by side and notice the pattern.

Use Horizontal and Vertical Analysis

Horizontal analysis looks at changes over time. Vertical analysis looks at how each line item compares as a percentage of revenue.

This matters because absolute figures can mislead. If revenue increased by 15 percent but payroll increased by 28 percent and marketing by 35 percent, that growth may not be helping much.

If the cost of goods sold is taking a larger share of revenue than it used to, your gross margin may be weakening even though sales look stronger.

This kind of analysis helps you move past surface-level performance and understand the quality of your numbers.

2. Evaluate Cash Flow Management

Cash flow is often the clearest test of a company’s financial health because it tells you whether the business can function in real life, not just on paper.

Why Operating Cash Flow Matters More Than Excitement

A business can be busy and profitable on paper, yet still face real strain if cash does not arrive at the right time.

Operating cash flow tells you whether core business activity is actually generating usable cash.

If your business regularly struggles to cover payroll, rent, inventory, taxes, or supplier payments, that is a serious issue even if sales are growing.

Cash flow problems create pressure fast because obligations do not care that an invoice was sent and might not get paid later.

Working Capital and Short-Term Obligations

A company’s working capital is the difference between its current assets and its current liabilities. In simple terms, it helps show whether the business can meet short-term obligations without stress.

A healthy working capital position gives breathing room. A weak one means the business may be surviving too close to the edge.

You may not feel this during strong months, but a single slow payment cycle or an unexpected cost can expose the weakness quickly.

Accounts Receivable, Inventory, and Payables

Many small businesses run into trouble because money gets stuck.

Accounts receivable may be growing because clients pay slowly. Inventory may be sitting too long and tying up cash.

Payables may be stretching because the business is delaying payments to suppliers just to stay afloat.

These are not just accounting details. They are practical signals of how efficiently money moves through the business.

If you are collecting slowly, stocking inefficiently, and paying late, cash flow stress usually follows.

Free Cash Flow and Business Flexibility

Free cash flow is the amount that remains after operating expenses and necessary capital expenditures. It matters because it shows how much real financial flexibility the business has left.

That remaining cash is what supports reinvestment, owner distributions, debt reduction, emergency protection, and future growth.

If free cash flow is consistently thin or negative, the business may be active but not truly strong.

3. Analyze Revenue and Profitability Trends

Revenue matters, but not all revenue is equally healthy. You need to examine not only whether sales are rising, but whether that growth is reliable, profitable, and sustainable.

Revenue Growth Consistency

Healthy revenue is not just big. It is dependable. A business with smooth, repeatable revenue usually has more stability than one with erratic spikes and long dry periods.

Look at whether your revenue comes from recurring clients, seasonal surges, one-off projects, or a few large accounts.

If the business depends heavily on a single client or product line, that concentration creates risk. Strong financial health usually includes more balanced revenue sources.

Net profit margin, operating margin, and gross profit margin

Profitability trends help you understand whether the business model is working efficiently.

Gross profit margin shows the percentage of revenue left after direct costs. Operating margin reflects the amount remaining after operating expenses.

Net profit margin shows what is left after all expenses are accounted for.

These margins matter because revenue growth without a healthy margin structure can create false confidence.

If sales keep increasing but gross margin keeps shrinking, the business may be working harder for less actual benefit.

Revenue Quality Matters Too

High revenue is not always high-quality revenue. Discount-heavy sales, low-margin projects, slow-paying clients, and revenue tied to unstable conditions may look good in a headline number while creating strain behind the scenes.

Revenue quality improves when sales are profitable, collectible, recurring where possible, and aligned with the business’s capacity.

4. Assess Financial Risk Exposure

A financially healthy business does not just perform well in good conditions. It also has some protection when conditions change.

Debt Burden and Coverage Capacity

Debt is not automatically bad, but it becomes dangerous when repayment pressure limits flexibility. Review how much debt the business carries, what the repayment terms are, and whether earnings can comfortably support those payments.

If debt service is eating too much operating income, that is a warning sign. The business becomes more vulnerable to any slowdown, surprise expense, or delayed receivable.

Liquidity Risk

The possibility that a company won’t be able to pay its debts on time is known as liquidity risk. A company may own assets, inventory, or equipment and still face liquidity stress if usable cash is too low.

This is why ratios like the current ratio and quick ratio matter. They help determine whether the business has sufficient near-term financial strength to withstand pressure.

Client, Supplier, and Market Dependence

Risk exposure also includes concentration risk. If one client accounts for a large share of revenue, one supplier controls key inputs, or one market shift could sharply weaken demand, the business is more exposed than it may appear.

A business becomes financially stronger when it reduces overdependence and builds more options.

External Shocks and Cost Pressure

Inflation, rising wages, shipping costs, taxes, interest rates, and sector-specific changes can all affect business health. A strong financial review should include not only internal performance but also external vulnerabilities.

If your margins are already thin, even a small rise in costs can create serious pressure.

Key Metrics to Measure Financial Health

While industries differ, a few metrics are especially useful for most businesses.

Liquidity Metrics

The current ratio shows whether current assets can cover current liabilities. The quick ratio goes further by focusing on more liquid assets. These ratios help show whether the business can manage near-term obligations.

Profitability Metrics

The efficiency with which the company converts revenue into profits is shown by the gross margin, operating margin, and net profit margin.

If these are declining over time, the business may be underpricing, under cost pressure, or operating inefficiently.

Solvency Metrics

Debt-to-equity helps show how leveraged the business is. Interest coverage helps show whether earnings are strong enough to cover interest obligations safely.

Efficiency Metrics

Inventory turnover, receivables turnover, and payable turnover show how efficiently money is moving through daily operations. Slow movement often creates cash strain even when demand is healthy.

Warning Signs Your Business May Be Financially Unhealthy

A few red flags deserve immediate attention.

If sales are increasing but cash is always tight, something is wrong. If late payments to vendors are becoming normal, that matters. If margins are getting thinner each quarter, that matters too.

If one or two customers account for too much of the total revenue, that creates fragility. If debt is growing faster than earning power, the business is becoming more exposed.

These signs do not always mean disaster, but they do mean the business needs a closer look now, not someday.

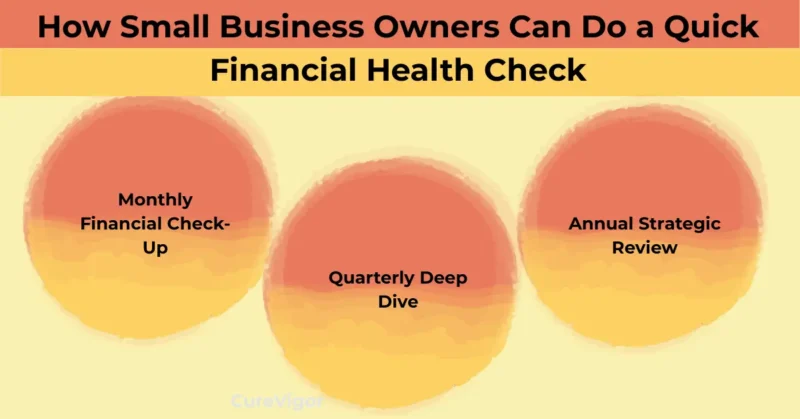

How Small Business Owners Can Do a Quick Financial Health Check

A strong business review does not need to be overly complicated, but it does need to be consistent.

Monthly Financial Check-Up

Once a month, review revenue, major expenses, cash on hand, receivables aging, upcoming payables, debt obligations, and margin movement. Check whether the business is on track or quietly drifting.

Quarterly Deep Dive

Once a quarter, review financial statements in more depth, compare results over time, analyze key ratios, evaluate pricing, and assess any emerging risks. This is the right time to ask whether the current model still works well.

Annual Strategic Review

Once a year, look at the bigger picture. Review growth plans, cost structure, owner compensation, financing needs, emergency reserves, and long-term sustainability.

This is also a good point for comparing your business’s financial health with your personal financial position.

If you want help on that side, your related post, How to Achieve Financial Stability and Prosperity, fits naturally here for founders, freelancers, and owner-operators whose business and personal finances closely influence each other.

Common Mistakes When Assessing Company Financial Health

Many owners make the same avoidable errors.

One is focusing only on revenue. Revenue is important, but it does not tell you whether the business is healthy. Another is confusing profit with cash flow. Profit can look fine while cash remains too tight to operate comfortably.

Another common mistake is skipping balance sheet analysis, which hides debt pressure, weak liquidity, and structural risk.

It is also risky to judge performance without trend comparison. One decent month does not erase a year of weakening numbers.

And finally, many businesses fail to compare their results against reasonable benchmarks for their size or industry.

Company Financial Health Checklist

Use this checklist as a practical review tool:

- I review my income statement, balance sheet, and cash flow statement regularly.

- I know my current cash position and upcoming obligations.

- I track receivables and know which invoices are aging.

- I understand my gross, operating, and net margins.

- I monitor debt levels and repayment pressure.

- I compare performance monthly, quarterly, and annually.

- I am not overly dependent on one client or supplier.

- My pricing still protects profitability.

- I know whether growth is actually improving cash flow.

- I have a plan for financial shocks or slow months.

If too many of these are unclear, the business needs more structure around financial review.

Recap on Assessing Company Financial Health

Checking your business’s financial health means looking beyond revenue to examine its real strengths.

- Company financial health shows how stable, efficient, and resilient a business really is beneath the surface.

- Revenue alone is not enough to judge business strength. Cash flow, profitability, debt, and liquidity matter just as much.

- The most effective way to assess company financial health is through four core steps: reviewing financial statements, evaluating cash flow, analyzing revenue and profit trends, and assessing financial risk.

- The income statement, balance sheet, and cash flow statement should always be reviewed together for a complete picture.

- Trend analysis helps reveal whether the business is improving, weakening, or maintaining financial stability over time.

- Strong operating cash flow is one of the clearest signs of a healthy business because it shows whether daily operations are generating real usable cash.

- Profit margins, working capital, receivables, inventory movement, and debt levels all help explain how well the business is functioning.

- Key ratios such as current ratio, quick ratio, gross profit margin, net profit margin, debt-to-equity, and receivables turnover can highlight strengths and warning signs.

- Common red flags include growing revenue with weak cash flow, shrinking margins, rising debt, late payments, and overdependence on a few clients.

- Regular financial reviews help business owners make better decisions earlier, before financial pressure becomes a crisis.

FAQs on Assessing Company Financial Health

Q. What is the best way to check a company’s financial health?

The best way is to review the three main financial statements together, then study cash flow, margins, debt levels, and short-term obligations. Looking at one number alone rarely tells the full story.

A strong business review combines performance, position, and risk. That gives you a much more honest picture of overall health.

Q. Which financial statement matters most?

No single statement should be used alone. The cash flow statement shows how money is actually moving, the balance sheet shows the financial position, and the income statement shows profitability.

If you had to give special attention to one, cash flow often deserves it, because many businesses fail from cash strain even when profits exist on paper.

Q. Can a profitable business still have poor financial health?

Yes, absolutely. A business can show profit while struggling with slow receivables, weak liquidity, rising debt, or unstable margins. Profitability matters, but it does not guarantee resilience.

Financial health depends on how the whole system works, not just whether the business earned money in a given period.

Q. How often should a business assess its company’s financial health?

To maintain strong company financial health, a light review should be conducted monthly, with a more in-depth analysis every quarter and a comprehensive strategic review once a year.

Businesses experiencing rapid growth or financial strain may need more frequent checks to stay ahead of potential issues. The key to maintaining good financial health is consistency; waiting until problems become obvious usually means.

They’ve already escalated, making them harder to address effectively. Regular assessments allow businesses to stay proactive and resilient.

Q. What are the biggest red flags in small business finances?

Major red flags include rising revenue but poor cash flow, repeated late payments, shrinking margins, heavy reliance on a few customers, and debt obligations that are becoming harder to manage.

These signs often point to structural issues rather than temporary bad luck. They should be treated seriously and reviewed early.

Q. What ratios indicate a company’s financial health?

Key ratios to assess company financial health include the current ratio, quick ratio, gross profit margin, net profit margin, debt-to-equity, and receivables turnover.

These ratios provide valuable insights into a company’s liquidity, profitability, debt levels, and operational efficiency.

They are most effective when tracked over time, as analyzing trends provides a clearer picture of financial stability and performance than relying on single-period data. Regular monitoring of these ratios helps detect early signs of financial stress or strength.

Q. What does company financial health mean, and why is it important?

Company financial health refers to the overall strength and stability of a business’s finances. It involves the company’s ability to generate cash, manage debts, maintain profitability, and meet both short-term and long-term obligations.

Regularly assessing a company’s financial health is critical because it helps identify potential risks and areas for improvement.

By understanding its financial position, a business can make informed decisions that support sustainable growth, maintain operational efficiency, and reduce the likelihood of financial crises. It also provides a clear picture for investors, lenders, and stakeholders.

Conclusion on Assessing Company Financial Health

A healthy business is not just one that sells. It is one that can support itself, meet its obligations, protect its margins, and adapt when conditions change. That kind of health does not come from guesswork or optimism. It comes from a regular, honest financial review.

Assessing company financial health is not just an accounting exercise. It is a practical way to determine whether your business is truly stable and sustainable, and able to support better decisions over time.

A company can appear active on the outside while carrying serious financial weakness underneath, which is why regular review matters so much.

When you look closely at financial statements, cash flow, profitability, and risk exposure, you move from assumption to clarity. That clarity helps you spot problems earlier, protect margins more effectively, manage obligations with more confidence, and make decisions based on evidence rather than pressure.

A healthier business is not simply one that earns more. It is one that can meet its commitments, manage its risks, and keep operating from a position of strength. The more honestly and consistently you assess your company’s financial health, the better your decisions become and the stronger your business foundation becomes.

Read more articles on Health and Wellness Tips.

You might like to read: