Financial stability and prosperity made simple. Actionable steps to achieve lasting financial health.

There is a particular kind of exhaustion that comes from always thinking about money.

It follows you through ordinary moments. Grocery shopping becomes mental math. A phone notification makes your stomach tighten because it might be a bill, a due date, or a balance reminder.

Even when things are not falling apart, there is a quiet fear that one mistake, one emergency, or one expensive month could push everything off track. Many people have lived in that state for years.

They earn, spend, worry, recover, repeat, and never quite feel secure.

That is why financial health matters so much.

Most people are not chasing luxury. They are chasing steadiness. They want enough control over their money to feel safe, enough breathing room to make thoughtful choices, and enough progress to believe the future might actually get easier.

Financial stability is what connects those goals. It is not a fantasy version of life where nothing goes wrong. It is a realistic system that helps you manage real life with more stability, less panic, and more options.

Prosperity begins there. Not with showy spending, not with pretending everything is under control, and not with the kind of fake financial confidence people perform online like it is a personality trait.

It begins with structure, awareness, and habits that help your money support your life rather than constantly interrupt it.

Quick Summary Box

- Financial stability means: having enough stability, control, and resilience in your money life to meet needs, handle setbacks, and move toward future goals.

- It is not the same as wealth: wealth is what you own, while financial stability reflects how well your finances actually function day to day.

- The foundations of financial stability: budgeting, debt control, emergency savings, long-term investing, protection, and regular review.

- Why it matters: financial stability supports peace of mind, flexibility, security, and long-term opportunity.

- What usually improves it fastest: tracking spending, building a starter emergency fund, reducing high-interest debt, and automating basic money habits.

- This guide will help you: understand financial stability, improve it step by step, and build long-term stability without fluff or unrealistic promises.

What This Guide Covers

This article explains what financial stability really means, why it matters, and how to achieve it through practical, realistic habits.

You will learn how financial health supports stability and prosperity, what signs show that your finances need attention, and which steps build stronger day-to-day control over money.

You will also find financial health goals worth working toward, common challenges that make progress harder, strategies for low- or irregular-income situations, a practical checklist, and answers to the questions people most often ask when they want to feel financially stronger.

If you want a broader explanation of the concept itself, you can naturally connect this post with Financial Health Defined: How to Measure and 7 Tips to Improve Your Own.

And if you run a company or side business, your related guide, How to Check the Financial Health of Your Business, fits well alongside this one.

What Financial Stability Really Means

Financial stability means having enough control over your money to handle everyday life without constant financial fear.

It is the ability to pay your essential expenses, stay on top of your obligations, absorb unexpected costs with less disruption, and make decisions from a place of clarity instead of panic.

It does not mean being rich or never facing financial pressure. It means your finances are steady enough that one difficult week, one surprise bill, or one temporary setback does not immediately throw everything into chaos.

Financial stability is built through consistency: reliable cash flow, manageable expenses, reduced dependence on debt, some emergency savings, and habits that help you stay in control over time.

In simple terms, financial stability is the point where money stops feeling like a constant emergency and starts feeling more manageable, predictable, and supportive of your life.

Financial Stability vs Financial Freedom vs Wealth

These terms are closely related, but they do not mean the same thing. People often use them interchangeably, yet each describes a different stage or dimension of financial life.

Financial stability is the foundation. It means your money is steady enough to cover your needs, handle normal disruptions, and support day-to-day life without constant stress.

You may still have limits, but your finances are not in a constant state of crisis. Stability is about control, consistency, and resilience.

Financial freedom usually means greater choice. It means your financial situation gives you more independence in how you live and work. You are less trapped by paycheck-to-paycheck pressure and more able to make decisions based on preference rather than necessity.

For some people, financial freedom means living off investments or passive income. For others, it simply means having enough savings, flexibility, and security to say no to unhealthy work or make major life choices with less fear.

Wealth is different from both. Wealth refers to the value of what you own, such as savings, investments, property, and other assets, minus what you owe. It is a measure of accumulation.

A person can have growing wealth on paper, but still lack financial stability if their cash flow is poor or their spending is out of control.

In the same way, someone can be financially stable without being wealthy, even if their assets are modest, as long as their finances are well-managed.

In simple terms, financial stability is about how well your money works, wealth is about how much you have built, and financial freedom is about how much choice your money gives you.

Stability helps you function, wealth helps you grow, and freedom helps you live with more flexibility.

Why Financial Stability Is the Foundation of Prosperity

Prosperity does not begin with excess. It begins with stability. Before people can build wealth, invest confidently, or make long-term plans.

They usually need a financial life that feels steady enough to support those decisions.

That is why financial stability comes first. It creates the conditions for real progress.

When money is constantly tight or unpredictable, most energy goes toward short-term survival. People focus on covering bills, avoiding late fees, juggling debt, or recovering from one setback after another.

In that kind of situation, prosperity stays out of reach not because the goal is unrealistic, but because instability keeps interrupting every attempt to move forward.

Financial stability changes that. It gives structure to your money life. It makes it easier to plan ahead, save consistently, reduce financial stress, and respond to problems without everything falling apart at once.

Stability creates breathing room, and that breathing room enables better decisions.

Prosperity grows from that stronger foundation. Once your finances are more stable, you can think beyond immediate pressure.

You can build savings, invest for the future, protect what you have, and make choices based on long-term goals instead of short-term fear.

In that sense, prosperity is not separate from stability. It is what stability makes possible over time.

Why Financial Health Matters

Financial health matters because money affects far more than purchases. It affects emotional energy, opportunities, relationships, and the sense of control you feel over your own life.

Stability and Security

One of the biggest benefits of financial health is basic stability. Stable finances mean bills are easier to manage, emergencies are less destructive, and the future feels less threatening.

Security does not always mean abundance. Often, it means knowing that one bad week will not undo your whole month.

Peace of Mind

Money stress is exhausting. It reduces focus, affects sleep, strains relationships, and makes ordinary decisions feel heavier than they should.

Better financial stability often brings something people deeply need but rarely describe well: mental quiet. That is worth more than most people realize.

Flexibility and Freedom

Financial stability gives you more options. You are more able to leave a bad job, handle a short income gap, support a family member carefully, or make a thoughtful long-term choice instead of a desperate short-term one. Financial freedom grows out of this kind of flexibility.

Opportunities for Growth

When your finances are more stable, you can think beyond immediate survival. You can invest, learn new skills, save for future goals, or pursue opportunities that require patience. Growth becomes more possible when money stops being a constant emergency.

Building Generational Stability

Building generational wealth is a popular phrase, but for many families, the more realistic starting point is building generational stability.

That means creating better habits, reducing financial chaos, teaching children practical money skills, and making decisions that leave the next generation with less confusion and more structure.

Signs Your Financial Health Needs Improvement

A lot of people know they are stressed about money, but they are less clear on what that stress is pointing to.

One sign is living paycheck to paycheck for long periods without building any cushion.

Another is using debt for essentials like groceries, transport, or utilities. Another is having no emergency fund despite months or years of income.

Constant late fees, vague awareness of spending, and avoiding financial accounts because they create anxiety are also signs that your money system needs attention.

A poor credit score, inadequate retirement savings, and lack of clear goals also matter, but the deeper issue is usually the same: money is being reacted to rather than managed with structure.

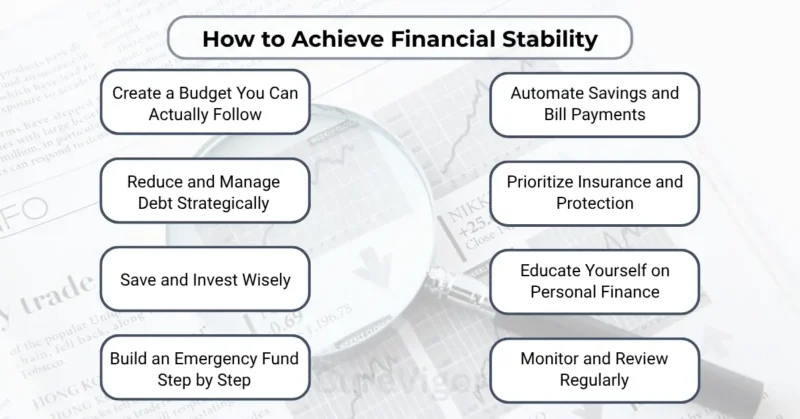

How to Achieve Financial Stability

Improving financial stability is not about one perfect plan. It is about building a system that works repeatedly in real life.

Create a Budget You Can Actually Follow

A budget is not supposed to make you feel restricted for sport. It is supposed to help you direct money where it needs to go.

A workable budget starts with honesty. Review what you actually spend, not what you wish you spent. Then separate essential expenses, important goals, and flexible spending.

Give every dollar a purpose. Housing, food, transport, debt payments, savings, family obligations, and basic enjoyment should all have a place.

Budgets become much more effective when they reflect reality rather than moral ambition dressed up as planning.

Reduce and Manage Debt Strategically

Debt becomes harmful when it steals too much of your monthly cash flow or keeps forcing future income to pay for past decisions.

High-interest debt should usually be handled first because it grows quickly and limits flexibility.

Choose a simple payoff strategy and stick to it. Some people are motivated by clearing smaller balances first.

Others prefer attacking the highest interest rate first. Either approach can work. The important thing is to stop adding to the problem while you are trying to reduce it.

Save and Invest Wisely

Saving protects your short-term stability. Investing supports your long-term future. Both matter.

Start with cash savings for emergencies and near-term needs. Once basic protection is in place, invest consistently in line with your goals, timeline, and risk tolerance.

Financial stability improves when saving and investing are treated as regular habits rather than occasional acts of discipline after a “good month.”

Build an Emergency Fund Step by Step

A strong emergency fund reduces panic and protects progress. Start small if you need to. A starter fund can still prevent borrowing for minor crises.

Over time, aim for a larger reserve that reflects your real responsibilities and income stability.

An emergency fund does not need to appear overnight. It needs to be built steadily and protected from being treated like extra spending money.

Automate Savings and Bill Payments

Automation is one of the simplest ways to improve financial stability because it reduces decision fatigue and missed deadlines.

Automatic transfers to savings, automatic bill payments, and automatic investing contributions create consistency even when life feels busy or messy.

Healthy financial systems rely less on motivation and more on structure. That is one of the most useful truths in personal finance.

Prioritize Insurance and Protection

Insurance is not exciting, which is exactly why people delay it until they need it and regret that delay in great detail.

Health insurance, life insurance (where relevant), income protection, and basic legal planning can all help protect financial stability. Financial stability is not just about growth. It is also about protection.

Continuously Educate Yourself on Personal Finance

You do not need to become a financial expert, but you do need enough understanding to make decent decisions.

Learn the basics of budgeting, debt, saving, investing, insurance, taxes, and credit. Better knowledge does not solve every money problem, but it helps you avoid expensive confusion.

Monitor and Review Regularly

Financial stability improves much faster when you review it regularly. A monthly check-in helps you track spending, savings, debt, and progress toward goals.

An annual review helps you reset larger priorities and adjust your plan after major life changes.

Financial Stability Goals Worth Working Toward

Goals create direction. Without them, money gets used up by whatever feels urgent in the moment.

Building an Emergency Fund

This should be one of the first goals for most people because it reduces reliance on debt and protects daily life from sudden disruption.

Paying Off Debt

Debt reduction improves flexibility and lowers monthly financial pressure. The more of your income you can keep for present needs and future goals, the healthier your finances become.

Saving for Retirement

Retirement savings matter even when they feel far away. The earlier you start, the more time you have on your side. Delaying for too long often means needing larger contributions later just to catch up.

Investing for Wealth Creation

Investing is how many people move beyond financial survival and begin building long-term prosperity. Wealth usually grows from time, consistency, and patience, not dramatic one-time decisions.

Achieving Financial Independence

Financial independence does not have to mean early retirement. For many people, it means reducing fear, increasing flexibility, and creating a life where money is less controlling.

Financial Health Strategies for Different Real-Life Situations

Not everyone is building financial health from the same starting point. Strategy matters more when circumstances are harder.

How to Improve Financial Health on a Low Income

Low income limits room for error, so priorities need to be sharper. Focus first on essentials, avoid late fees, reduce expensive debt, and build even a small emergency cushion. Progress may be slower, but it still matters.

Financial health on a low income often begins with stabilization, not optimization.

Managing Irregular Income

Irregular income creates stress because cash flow becomes less predictable. In this case, budgeting should be based on your lower-income months, not your best months.

During strong months, save the difference to smooth out weaker periods. A separate buffer account becomes especially useful here.

Handling High Living Expenses

When costs rise faster than income, financial pressure increases even if you are “doing everything right.” In these cases, review housing, transport, subscriptions, food spending, and fixed obligations carefully.

Some costs are non-negotiable, but many stay in place simply because they were never reassessed.

Recovering After a Financial Emergency

Financial emergencies can leave people feeling like all progress has been erased. The first job after a setback is not perfection.

It is stabilization. Cover essentials, stop the bleeding, rebuild small reserves, and create a plan for the next few months. Recovery works best when it is practical, not dramatic.

Supporting Family Without Losing Your Own Stability

Many people want to help financially with their parents, siblings, or children. That can be generous, but it needs structure.

Decide what you can afford, what kind of help is sustainable, and where your own boundaries need to stay. Support should not quietly destroy your own financial health in the background.

Common Financial Health Challenges

Even with good intentions, a lot can get in the way.

Limited income makes everything harder because there is less flexibility. High living expenses reduce savings potential. Unplanned emergencies interrupt momentum. A lack of financial literacy leads to costly mistakes or to avoidance.

Impulsive spending creates leaks that feel small in the moment but large over time. Overreliance on debt puts future income under pressure and makes recovery harder.

Naming these challenges matters because they help explain why improvement can feel difficult. Financial health is not only about discipline. It is also shaped by circumstance, knowledge, and timing.

Common Financial Health Issues

Some issues appear repeatedly across households.

A poor credit score can raise borrowing costs and reduce options. Inadequate retirement savings create long-term vulnerability. Living beyond your means makes every month feel tighter than it should.

Lack of emergency savings increases dependence on credit. Lack of financial goals leaves spending directionless.

These issues are common but workable. Most of them improve when a better structure is applied consistently.

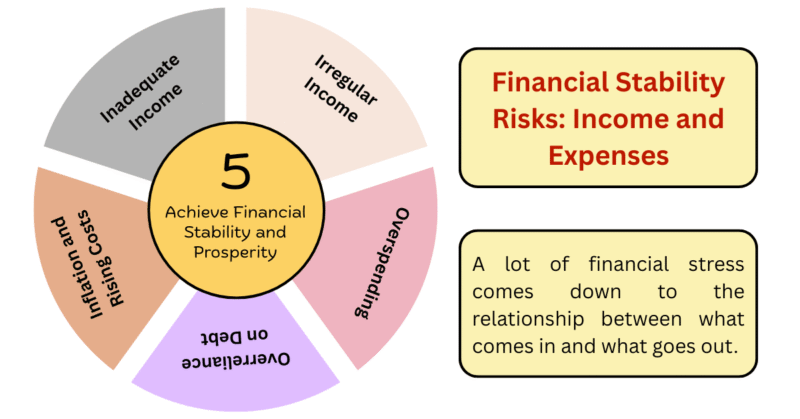

Financial Stability Risks: Income and Expenses

A lot of financial stress comes down to the relationship between what comes in and what goes out.

Inadequate Income

Sometimes the core issue really is not spending. The income is too low to cover basic living costs. In this case, a financial health strategy may need to include skill-building, side income, rate increases, job changes, or household restructuring.

Irregular Income

Unpredictable income makes planning difficult, even when total annual earnings appear acceptable. This is why cash reserves and conservative budgeting matter so much for freelancers, contractors, and seasonal earners.

Overspending

Overspending does not always look reckless. Often, it hides in emotional spending, convenience spending, or slow lifestyle creep. These patterns matter because they reduce room for savings and keep financial stress high.

Inflation and Rising Costs

Even disciplined people feel pressure when essentials become more expensive. When costs rise, your money plan has to adjust. Old budgets do not solve current conditions.

Overreliance on Debt

Debt becomes a major risk when it supports everyday living instead of temporary, manageable borrowing. Once basic living expenses are funded through credit, financial health usually weakens quickly.

Habits That Build Long-Term Stability and Prosperity

Long-term financial improvement usually comes from boring habits done consistently. Annoying, really. Humans always want a breakthrough, only to be quietly saved by routines.

Paying yourself first helps savings happen before spending expands. Tracking net worth over time helps you see bigger progress, not just monthly frustration.

Setting short-, mid-, and long-term goals creates direction. Diversifying income streams can improve resilience. Seeking professional advice can help when decisions become more complex or repeated mistakes keep happening.

These habits may look simple, but they are powerful because they strengthen both control and resilience.

A Practical Financial Health Checklist

Use this checklist to assess your current position:

- I know how much money comes in each month.

- I know my essential monthly expenses.

- I follow a workable budget.

- I pay bills on time most months.

- I am reducing or controlling high-interest debt.

- I have at least a starter emergency fund.

- I save or invest consistently.

- I have clear short- and long-term money goals.

- I review my finances regularly.

- My money habits support stability, not just survival.

If several of these are missing, that is not a verdict. It is a map. It shows where attention is needed first.

Recap

Achieving financial health is about building stability, reducing unnecessary strain, and creating a money system that supports both present needs and future goals.

It starts with clear awareness, then grows through budgeting, debt control, emergency savings, smart investing, protection, and regular review.

Financial prosperity is not built only through higher income. It is built through stronger habits, better decisions, and a more resilient financial foundation. The goal is not a perfect financial life. The goal is a healthier one.

FAQs

Q. What does it mean to achieve financial health?

Achieving financial health means reaching a point where your finances are stable enough to support your daily needs, protect you from common setbacks, and help you move toward future goals. It does not require being wealthy.

It requires structure, awareness, and habits that keep your money working steadily and reliably.

Q. How long does it take to improve financial health?

That depends on your starting point, income level, debt burden, and consistency. Some improvements, like budgeting better or stopping late fees, can happen quickly.

Bigger improvements, such as building emergency savings or paying down major debt, often take longer. What matters most is steady direction, not instant transformation.

Q. What should I do first if my finances are a mess?

Start by getting clear. List your income, essential expenses, debts, due dates, and current balances.

Then stabilize the basics by covering essentials, avoiding new high-interest debt, and building a small emergency cushion if possible. Clarity comes before strategy. Without it, you are solving stress with guesswork.

Q. Is financial health possible on a low income?

Yes, but it often looks different and takes longer. On a low income, financial health may begin with avoiding late fees, reducing debt dependence, protecting essentials, and building a small reserve rather than aiming immediately for large savings or major investing. Progress still counts, even when the pace is slower.

Q. What is the 70/20/10 money rule?

The 70/20/10 rule is a simple budgeting framework in which 70 per cent of income goes to living expenses, 20 per cent to savings or debt repayment, and 10 per cent to giving or personal priorities.

It can be useful as a rough guide, but it should be adjusted to fit real income, cost of living, and goals.

Q. What is the 3 6 9 rule in finance?

The 3-6-9 rule usually refers to emergency savings targets. It often means aiming for 3 months of expenses as a minimum buffer, 6 months for stronger protection, and 9 months if income is unstable or responsibilities are higher.

It is a practical guideline, not a strict law, but it helps people think in realistic stages.

Conclusion

Financial health is not something reserved for people with perfect salaries, perfect discipline, or perfect timing. It is built by people who decide to understand their money more honestly and handle it with more intention.

That process can start small. A clearer budget. One automatic transfer. One debt payoff plan. One month of paying attention instead of avoiding.

Those small actions matter because they create momentum, and momentum changes how money feels. Over time, stability grows.

Stress softens. Choices expand. That is what prosperity looks like in real life. Not just having more, but feeling stronger, steadier, and less controlled by fear.

If you want the wider measurement framework behind this topic, connect this post with Financial Health Defined: How to Measure and 7 Tips to Improve Your Own. And if you also run a company, pair it with “How to Check the Financial Health of Your Business” so both your personal and business finances are built on a healthier foundation.

If this article reflects where you are right now, share your thoughts, your biggest financial challenge, or the habit you are trying to build next.

Honest money conversations are more useful than pretending everyone has it figured out.

Read more articles about Health & Wellness Tips.

You might enjoy reading: