Learn how to achieve financial success without sacrificing your peace. Master the 5 pillars of stress-free wealth building, automate your systems, and design a life of true freedom and balance.

Most people spend years chasing a number. A salary target. A savings milestone. A net worth figure they once read somewhere and quietly adopted as the finish line.

And then, when they get close, or even when they cross it, something unexpected happens. They don’t feel the way they thought they would.

The anxiety is still there. The restlessness hasn’t gone. The sense of never quite having enough hasn’t eased. They’re more financially successful by almost any external measure, and yet the stress hasn’t left the room.

This is more common than most financial content admits. And it points to something worth saying clearly: financial success, as it’s traditionally defined, is incomplete. The number matters, of course, it does, but it doesn’t tell the whole story.

Real financial success includes how you feel about your money. It includes how freely you can make decisions, how much of your time and energy you actually own, and whether the life you’re building financially is the life you actually want.

This article is for anyone who suspects there’s more to the picture than their bank balance shows. It won’t promise an overnight transformation or sell you on a secret formula.

It will give you an honest, grounded framework for thinking about financial success differently, and for building it in a way that’s sustainable, human, and genuinely worth having.

Quick Summary

What this article covers:

This article explains why the traditional definition of financial success leaves people stressed and unfulfilled.

It covers five mindsets working against your financial well-being, five foundational pillars of a strategy that holds up, and seven practical strategies for building financial success without burning out.

It also covers the often-overlooked role of systems, self-care, and long-term thinking.

Anyone working hard financially but still feeling like something important is missing, whether that’s clarity, calm, direction, or simply a sense that they’re building something that matters.

Financial success isn’t a destination with a fixed dollar amount. It’s a relationship between your money, your values, your time, and your well-being. Getting that relationship right changes everything.

Redefining Financial Success: Time, Energy, and Freedom

The standard definition of financial success is largely inherited. It comes from cultural messaging, family patterns, social comparison, and decades of financial media that equate success with accumulation. Earn more. Save more. Invest more. Spend less. Repeat until wealthy.

That framework isn’t wrong, exactly. But it’s dangerously incomplete. It focuses almost entirely on inputs and outputs, income, assets, and net worth, and nearly ignores the human experience of managing money over a lifetime.

It doesn’t account for the toll that financial stress takes on health and relationships. It doesn’t ask whether the money you’re accumulating is actually buying the life you want.

And it rarely addresses the psychological dimensions of financial behavior, the fear, the avoidance, the comparison, the shame, that quietly shape financial outcomes far more than most people realize.

True financial success has three dimensions that the traditional definition misses.

The first is Time.

Money that costs you every waking hour to maintain isn’t freedom. It’s a more comfortable form of captivity.

A meaningful measure of financial success has to include how much time you have for the things and people that matter to you.

The second is Energy.

Chronic financial stress drains cognitive and emotional resources. Your ability to be creative, connected, and joyful is reduced when a large amount of your mental capacity is taken up by financial anxiety, the background hum of debt, insecurity, or unclear goals.

Real financial success reduces that drain. It doesn’t just increase the income that supposedly makes the drain worthwhile.

The third is Freedom.

Specifically, the freedom to make choices that align with your values. Not perfect choices. Not unlimited choices. But a genuine sense that your financial situation supports the life you’re trying to live, rather than constantly working against it.

Key Takeaways

Financial success is not a single number. It includes time, energy, and freedom alongside net worth.

The stress many people feel around money often comes from mindset patterns, not just financial circumstances. Building financial success sustainably requires both practical strategy and psychological self-awareness.

Small, consistent progress creates more lasting well-being than dramatic financial moves that can’t be maintained.

Common Misconceptions About Financial Success

Several deeply held beliefs about money quietly create stress while masquerading as wisdom. They’re worth naming directly.

Misconception one: More income automatically means less financial stress. It often doesn’t. Spending, anxiety, and financial behavior tend to scale with income unless intentionally managed.

Many high earners are more financially stressed than people with modest but stable incomes. Their lifestyle costs and financial obligations have expanded in lockstep with their earnings.

Misconception two: Financial struggle is a character flaw. It isn’t. Financial behavior is shaped by upbringing, education, psychological history, and circumstances that have nothing to do with intelligence or effort.

Understanding this removes shame from the equation. And shame, as it turns out, is one of the biggest obstacles to making real financial change.

Misconception three: Financial success requires the sacrifice of everything else. It doesn’t.

The most durable forms of financial progress are built around habits that integrate naturally into real life, not extreme deprivation that collapses under normal human pressure.

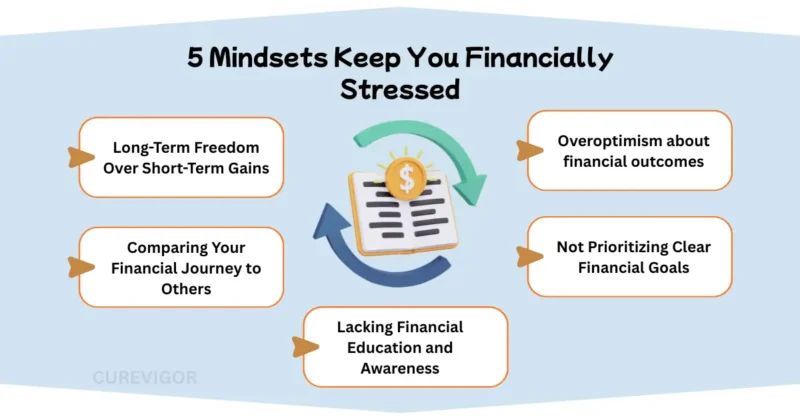

5 Mindsets Keep You Financially Stressed

Long-Term Freedom Over Short-Term Gains

Short-term financial thinking isn’t laziness or irresponsibility. It’s often a completely rational response to genuine uncertainty.

When money is tight or when the future feels unpredictable, focusing on immediate needs makes sense.

The problem arises when short-term thinking becomes a permanent default, even after circumstances have stabilized.

The financial cost of short-term thinking is well-documented. It leads to high-interest borrowing, deferred saving, reactive decision-making, and missed compounding opportunities.

The psychological cost is equally significant. Living in constant financial reaction mode, managing crises as they arise rather than building toward something, is exhausting. It keeps the nervous system in a low-grade state of alert, eroding well-being over time.

Shifting toward longer-term thinking doesn’t require certainty about the future. It requires building even small buffers, financial and psychological, that create enough stability to look beyond the next pay cycle.

A three-month emergency fund, however modest, is not just a financial tool. It’s permission to think further ahead.

Comparing Your Financial Journey to Others

Financial comparison is one of the most reliable generators of misery that modern life has to offer. It was always a problem.

Social media has made it significantly worse. It provides a constant, curated stream of other people’s financial highlights while hiding their struggles, debts, and anxieties entirely.

The research on social comparison and financial behavior is fairly detailed.

People who frequently compare their financial situations to those of others report higher levels of anxiety, lower life satisfaction, and a greater tendency toward spending that doesn’t reflect their actual values.

They spend more on things they don’t really want, in pursuit of a version of success that isn’t really theirs.

The antidote is not to be indifferent to what others have. That’s an unrealistic ask. It’s to develop a clearer picture of your own values and financial goals, specific enough that external benchmarks lose some of their power.

When you know what you’re actually working toward and why, other people’s timelines and milestones become less relevant.

Lacking Financial Education and Awareness

There’s a remarkable gap between the complexity of modern personal finance and the financial education most people receive growing up.

Compound interest, tax-advantaged accounts, debt structures, investment vehicles, and insurance products, none of these is taught reliably or consistently.

The result is that millions of adults are making high-stakes financial decisions with incomplete or inaccurate mental models.

This knowledge gap creates a specific kind of stress: the anxiety of not knowing what you don’t know.

Financial decisions can feel overwhelming, not because they’re inherently that complex, but because the concepts underlying them are unfamiliar.

Avoidance is a natural response to that overwhelm. And avoidance makes everything worse.

Improving financial literacy doesn’t require a finance degree. It requires consistent, accessible learning. Finding one or two reliable sources. Spending even 20 minutes a week on financial education.

Gradually building a vocabulary that makes financial decision-making feel less threatening. Knowledge reduces uncertainty. Reduced uncertainty reduces stress.

Being Overly Optimistic About Financial Outcomes

Optimism is generally a psychological asset. But in financial planning, uncalibrated optimism is a quiet liability.

Assuming income will keep rising, that investments will perform above average, and that no unexpected expenses will arise, these assumptions lead to plans that are fragile and goals that repeatedly disappoint.

The stress that comes from this kind of optimism is cumulative. Each time reality falls short of an optimistic projection, it generates frustration and discouragement. Often, it causes a retreat from financial planning altogether.

The cycle goes like this: set an ambitious goal, fall short, lose motivation, set another ambitious goal.

Realistic financial goals account for irregular expenses, modest rather than exceptional investment returns, and genuine friction in behavior change. These plans survive contact with real life.

They may look less impressive on paper. But they’re far more likely to actually work.

Not Prioritizing Clear Financial Goals

Vague financial intentions, “I want to save more,” “I should pay down debt,” “I need to be better with money,” share a common problem.

They provide no direction and no way to measure progress. Without those two things, motivation is nearly impossible to sustain.

Financial stress feeds on vagueness. When goals are unclear, every financial decision becomes a judgment call with no reference point. Spending feels either permissible or guilty, with nothing in between.

The uncertainty of not knowing whether you’re on track, because there’s no track to be on, creates a low-level anxiety that doesn’t resolve until a clear direction is established.

Setting a specific, time-bound financial goal, even one modest goal, creates structure.

It turns financial management from an overwhelming abstraction into a directed activity with a clear purpose. That shift in psychological experience is significant, independent of the goal itself.

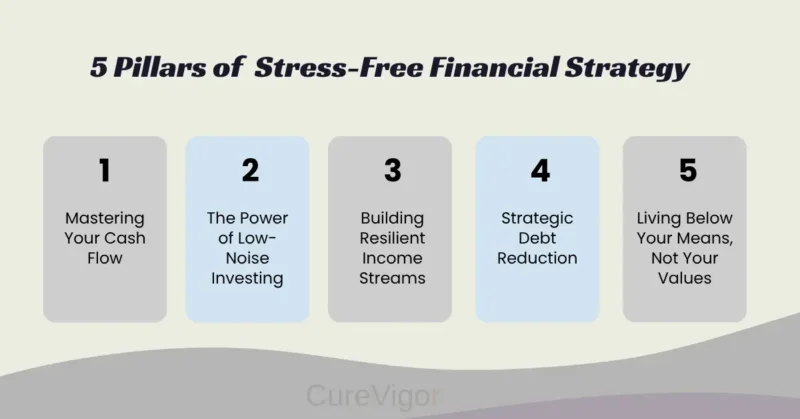

5 Pillars of a Stress-Free Financial Strategy

Mastering Your Cash Flow

Everything in personal finance begins with cash flow, the relationship between what comes in and what goes out. It sounds elementary.

But a surprising number of people manage their finances by feel rather than by fact.

They have a general sense of their income and a rough idea of their spending, but not a clear, current picture of where their money actually goes each month.

Mastering cash flow is not about obsessive tracking or punishing budgets. It’s about having enough clarity to make intentional decisions.

That means knowing your fixed costs, understanding your variable spending patterns, and identifying the gaps where money disappears without a clear purpose.

That clarity alone, without changing a single spending behavior, tends to reduce financial anxiety noticeably.

Because uncertainty is replaced by knowledge. Once you know your cash flow clearly, you can direct it deliberately.

You can see where adjustments are possible, which expenses align with your values, and which are mainly driven by habit.

The Power of Low-Noise Investing

Investment stress is a particular phenomenon worth addressing directly. Many people experience investing as inherently anxiety-producing.

Watching markets move, second-guessing allocations, wondering whether to act on news or ignore it.

This anxiety leads to one of two equally problematic responses: paralysis, meaning not investing at all, or reactivity, meaning making emotionally driven changes that undermine long-term returns.

Low-noise investing is a deliberate approach to removing this source of stress. It means choosing investment strategies that require minimal ongoing attention.

Broadly diversified, low-cost index funds held over long periods, for example. And then, as far as possible, leaving them alone.

It means not checking portfolio values daily. It means having a clear investment policy that removes most decisions from the realm of emotion.

The evidence strongly supports this approach, not just psychologically but financially. Most active investment decisions made in response to market movements reduce returns rather than improving them.

Simplifying your investment approach is not a concession. It’s often a genuinely better strategy.

Building Resilient Income Streams

Income from a single source is financially and psychologically fragile. When that one source is disrupted, through job loss, illness, industry change, or economic downturn, the entire financial situation becomes vulnerable.

That vulnerability creates a background anxiety that’s difficult to fully suppress, even when the primary income source feels stable.

Building additional income streams, whether through a side skill, rental income, freelance work, dividend income, or a small business, doesn’t just improve the financial picture; it also helps build wealth. It also helps build wealth. It reduces the psychological weight of depending entirely on one source.

Knowing you have other sources of income frequently reduces stress more than the secondary income’s actual monetary value.

The process doesn’t need to be dramatic. Many people start with a skill they already have, offered in a different context.

The goal in the early stages is not significant additional income. It’s the resilience and confidence that even a modest secondary stream provides.

Strategic Debt Reduction

Debt is one of the most reliably stress-producing financial conditions. Not just because of its financial cost, but because of its psychological weight.

The awareness of owing money, the compounding interest that grows whether you engage with it or not, and the sense of financial limitation it creates are constant sources of low-grade anxiety for millions of people.

Strategic debt reduction means approaching debt with a clear plan rather than a sense of helpless obligation.

It means knowing which debts to prioritise, understanding what each one actually costs you, and making consistent progress, however incremental, toward reducing them.

Two approaches dominate. The avalanche method focuses on the highest-interest debt first. It’s mathematically optimal and saves the most money over time. The snowball method focuses on the smallest balance first.

It builds momentum through early wins. Neither is universally correct. The right choice depends on your psychology as much as your numbers. Because the best debt strategy is the one you’ll actually sustain.

Living Below Your Means, Not Your Values

“Live below your means” is advice that’s technically correct but often lands poorly. It sounds like a permanent instruction to deprive yourself. That’s not what it needs to mean.

A more useful framing: spend less than you earn, but make sure what you spend genuinely reflects what you value.

The goal is not austerity. It’s alignment. Spend generously on the things that genuinely improve your life. Be indifferent to the things that don’t. Rather than spending unconsciously on everything and feeling vaguely guilty about all of it.

This reframe matters because it makes sustainable financial behavior psychologically possible. Deprivation-based approaches generate resentment and collapse.

Value-aligned spending generates something closer to satisfaction, the sense that your money is actually working in service of your real life.

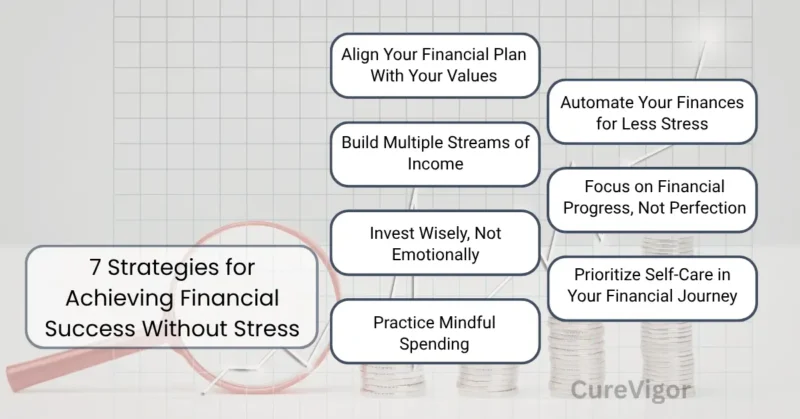

7 Strategies for Achieving Financial Success Without Stress

Align Your Financial Plan With Your Values

A financial plan that doesn’t reflect your actual life is a plan you won’t follow. The plans most likely to fail are built around idealized behavior, perfect discipline, zero friction, maximum optimization, rather than realistic human beings with irregular lives and competing priorities.

Building a financial plan that works starts with clarity about values. What do you actually want your money to do for you? Security? Freedom? Experiences? Stability for your family? Early retirement?

The ability to give generously? When you’re clear on this, financial decisions become much easier to make. Because you have a reference point that isn’t someone else’s benchmark.

From there, the plan itself can be simple. Track income and expenses. Set one or two clear savings goals.

Assign your money a direction before it arrives, rather than managing the aftermath of where it went. Review it periodically and adjust when life changes, because it will.

Build Multiple Streams of Income

The most financially secure people are rarely dependent on one thing going right. They’ve built, over time, a portfolio of income sources that creates resilience. So that when one stream is disrupted, the whole structure doesn’t collapse.

This isn’t just for entrepreneurs or high earners. Most people have skills, knowledge, or assets that could generate additional income at a modest scale.

The key is starting before you need it, building secondary income streams from a position of stability rather than desperation.

The psychological benefit arrives early, often before the financial benefit does. Knowing you have options, that your financial situation isn’t entirely contingent on a single employer’s decisions, changes how you carry yourself and how much mental energy you spend on financial anxiety.

Invest Wisely, Not Emotionally

Emotional investing is one of the most reliable ways to undermine financial success. It’s the pattern of buying when optimism is high and selling when fear takes over. This consistently produces the opposite of what investors intend.

The solution is not to remove all emotion from financial decisions. That’s not how human beings work. It’s to build structures that reduce the role of emotion in routine investment decisions.

Automated contributions. A clear written investment policy. A long enough time horizon that short-term volatility becomes less threatening. A commitment to not checking account values during market downturns.

Wise investing is mostly about not doing harmful things, rather than doing brilliant things. Consistency, patience, and low costs produce better outcomes for most people than active management and reactive decisions.

Practice Mindful Spending

Mindful spending is a practice, not a restriction. It means bringing conscious awareness to financial decisions.

Pausing to ask whether a purchase reflects what you actually value, rather than buying on autopilot and reconciling with the results later.

In practical terms, this might look like a 24-hour pause on non-essential purchases above a certain amount.

It might look like a monthly review of spending that’s curious rather than judgmental, focusing at where the money went and whether it aligns with your stated priorities.

It might look like learning to distinguish between purchases that bring genuine, lasting satisfaction and those that provide momentary relief followed by regret.

None of this requires extreme frugality. Mindful spending is compatible with spending generously, on the things that genuinely matter to you. It simply requires that spending be intentional rather than on autopilot.

Automate Your Finances for Less Stress

Every financial decision that depends on willpower is a potential source of failure. Human willpower is real but finite. It degrades under stress, fatigue, and distraction, precisely the conditions that financial difficulty tends to produce.

Automation removes willpower from the equation for your most important financial behaviors.

Savings are transferred automatically before you see the money in your checking account.

Debt payments are scheduled so you never accidentally miss them. Investment contributions happen regardless of whether you’re feeling financially motivated that month.

The psychological relief of automation is often underappreciated.

When your financial fundamentals are in place and saving and debt reduction occur consistently without requiring a decision at each cycle, the cognitive and emotional load of managing money decreases significantly.

That mental space is not trivial. It’s part of what financial freedom actually feels like.

Focus on Financial Progress, Not Perfection

Financial perfectionism, the belief that a deviation from the plan is a failure that undermines everything, is one of the quietest but most consistent obstacles to long-term financial progress.

It turns the inevitable friction of real financial life into a series of perceived failures. And failures tend to generate avoidance.

Every financial journey includes months where spending exceeds the plan, unexpected expenses that disrupt savings goals, and decisions made under pressure that would look different in hindsight. This is normal. It is not evidence of permanent failure.

What matters is the trend over a meaningful period, six months, a year, or five years.

A simple visual of that trend, a savings balance growing, a debt total declining, net worth moving in the right direction, makes progress visible in a way that day-to-day management can’t.

And visible progress, even slow progress, is one of the most effective motivators available.

Prioritize Self-Care in Your Financial Journey

There is a reciprocal relationship between personal and financial well-being. Financial stress undermines physical and mental well-being.

But poor physical and mental health, burnout, chronic stress, anxiety, and depression also undermine financial decision-making. The self-care connection in financial planning is not a soft add-on. It’s a practical requirement.

This means protecting sleep, because sleep-deprived people make financial decisions that are measurably worse.

It means managing stress through whatever approaches are accessible, such as physical activity, time in nature, meaningful social connection, because chronic stress impairs the clear thinking that good financial management requires.

It also means recognizing when financial anxiety has grown large enough to warrant professional support, whether from a financial therapist, a counselor, or a trusted advisor.

Taking care of yourself is not separate from financial success. It is one of the conditions that makes it possible.

The Systems of Financial Success

Automating Your Financial Routine

Systems matter more than motivation in personal finance. Because motivation fluctuates, and systems don’t. A financial system is simply a set of structures that enable consistent, effortless financial behavior.

The most effective financial systems share a few characteristics. They reduce decision points. Fewer choices to make means fewer opportunities for the wrong choice.

They make desired behaviors the path of least resistance. Saving is automatic, investing is scheduled, and bills are paid before discretionary spending begins.

And they include simple feedback mechanisms that let you see how you’re doing without requiring elaborate tracking.

Building even one or two of these systems, such as an automatic savings transfer, a monthly calendar reminder for a financial check-in, creates more lasting improvement than many more dramatic financial resolutions.

Setting High-Impact, Realistic Goals

Not all financial goals are created equal. Some create momentum and clarity. Others generate either complacency, if they’re too easy, or discouragement, if they’re too ambitious.

High-impact financial goals share a few consistent characteristics. They’re specific enough to be measurable, not “save more” but “save $300 per month.”

They’re meaningful, connected to something that genuinely matters rather than an arbitrary benchmark. They’re realistic given current circumstances. And they have a clear timeline that creates focus without unnecessary pressure.

Starting with one clear, achievable goal, rather than a comprehensive financial overhaul, produces better outcomes than plans that overwhelm from the start.

The first goal builds both financial progress and the habit of goal-directed financial behavior.

Building a Professional Support System

There’s a persistent cultural message that capable adults should manage their finances independently. It’s worth questioning. Financial planning is genuinely complex. Tax laws change.

Investment options multiply. The psychological dimensions of money management are beyond what most people can navigate on their own, and they have blind spots.

A financial advisor, credit counselor, or financial therapist isn’t a luxury reserved for the wealthy. They’re a resource that, used well, can pay for itself many times over.

Not just financially, but in reduced stress and better decision-making. The key is finding professionals whose interests are aligned with yours, fee-only advisors rather than commission-based, for example, and who treat you as a capable participant in your own financial planning.

For those with limited budgets, nonprofit credit counseling agencies offer genuine expertise at low or no cost.

Online tools and communities provide education and accountability. The point is that you don’t have to figure this out entirely alone. And the belief that you should is one of the things that worsens financial stress.

The Self-Care Connection: Mental Wellness as a Wealth Strategy

Somewhere along the way, personal finance and personal well-being got separated into different conversations.

Finance was about numbers, strategy, and discipline. Well-being was about feelings, mindfulness, and self-care. The two were rarely discussed together.

That separation has been costly. The evidence now clearly connects mental and emotional health to financial outcomes. Not as vague inspiration, but as a practical, causal relationship.

People who manage their stress effectively make better financial decisions. People who sleep well have more capacity for financial planning.

People who address psychological obstacles to financial behavior make more lasting financial progress than those who treat finance as purely a numbers problem.

Mental wellness is not separate from your financial strategy. In many ways, it is your financial strategy.

Protecting Your Time and Energy

Time and energy are the two most undervalued resources in most financial conversations. The financial decisions that look optimal on paper often make terrible sense when you factor in the real human costs.

The extra hours worked at the expense of health and relationships. The side hustle that generates income while gradually creating burnout. The aggressive savings plan leaves no room for the experiences that make a life feel worthwhile.

Building financial success without burning out requires treating time and energy as assets to be protected, not unlimited inputs to be maximized.

This means making intentional choices about where you direct your effort. The financial plan that’s 10% less aggressive but 50% more sustainable will almost always outperform the optimal plan you can’t maintain.

Success Without the Burnout

The version of financial success that requires chronic overwork, permanent sacrifice, and the suppression of everything enjoyable until some future date of arrival is not a strategy.

It’s a form of self-punishment that rarely leads to the promised destination.

Sustainable financial success is built on habits that can be maintained through good years and difficult ones, through life changes and unexpected events, through the full complexity of a real human life.

That sustainability requires leaving enough margin, financial, temporal, and emotional, to absorb setbacks without collapse.

Burnout, in this context, isn’t just a personal well-being concern. It’s a financial risk. When the strategy that was supposed to build your financial future becomes the thing that depletes your capacity to execute it, something has gone wrong.

Building at a pace that’s sustainable isn’t settling for less. It’s the more intelligent approach.

Achieving Financial Success on Your Own Terms

Quality of Life vs Quantity of Stuff

The research on money and happiness is fairly consistent on one point. Beyond a threshold of genuine security and comfort, additional wealth produces diminishing returns on well-being.

The relationship between more money and more happiness flattens out. Not immediately, and not for everyone, but reliably enough to suggest that the pursuit of ever-increasing accumulation has limits as a primary life strategy.

What continues to produce well-being well beyond that threshold: strong relationships, meaningful work, a sense of autonomy and purpose, good health, and the freedom to spend time in ways that reflect your values.

None of these is purely a financial achievement. Some of them require money to support. None of them is simply reducible to it.

This isn’t an argument against financial ambition. It’s an argument for asking, periodically, whether the financial goals you’re pursuing are actually connected to the life you want.

Or whether they’ve become goals in their own right, disconnected from the quality of life they were originally meant to serve.

Designing a Legacy of Freedom

The word “legacy” often comes up in conversations about inheritance and estate planning. But it’s worth using in a broader sense here. The financial life you build is not just a set of present-day decisions.

It’s a pattern of behavior, values, and habits that extends forward in time and, for those with people who matter to them, outward into other lives.

Financial freedom, the condition of having enough stability, flexibility, and alignment between your resources and your values to live on your own terms, is among the most meaningful things a person can build over a lifetime.

It doesn’t require exceptional wealth. It requires intention. A clear enough sense of what matters to you that your financial decisions, made consistently over time, move you toward it rather than away from it.

The starting point is almost never the important thing. The direction and consistency are.

The Bottom Line: Your Path to Stress-Free Financial Success

Financial success is not a fixed destination. It’s not a net worth number, an income level, or a specific asset target. It is the condition of having your financial life working in genuine support of your real life.

With enough security to feel stable, enough flexibility to make meaningful choices, and enough alignment between your money and your values that financial management feels purposeful rather than punishing.

Getting there requires both practical strategy and honest self-awareness. It requires identifying the mindset patterns that generate stress and replacing them with clearer, more grounded perspectives.

It requires building systems that make good financial behavior sustainable, not just occasional. And it requires understanding that your well-being and your financial health are not competing priorities. They are interdependent.

None of this is quick. But almost all of it is within reach for most people, starting from wherever they are now.

The path doesn’t require perfection. It requires direction, consistency, and the willingness to build something real rather than perform something impressive.

That is what financial success, honestly defined, actually looks like.

Financial situations vary significantly. If you’re navigating significant debt, financial hardship, or money-related anxiety, consider connecting with a nonprofit credit counsellor or financial therapist. Seeking professional advice does not indicate failure. It’s among the best tools out there.

Get more Health & Wellness Tips.

You might like to read: